A Battle in ERCOT over Colocation, PJM Withdrawals, 28.2 GW of New APS Activity, and More

Here's your roundup for the most important factors impacting the grid over the past two weeks

What happened from May 30 - Jun 12, 2026

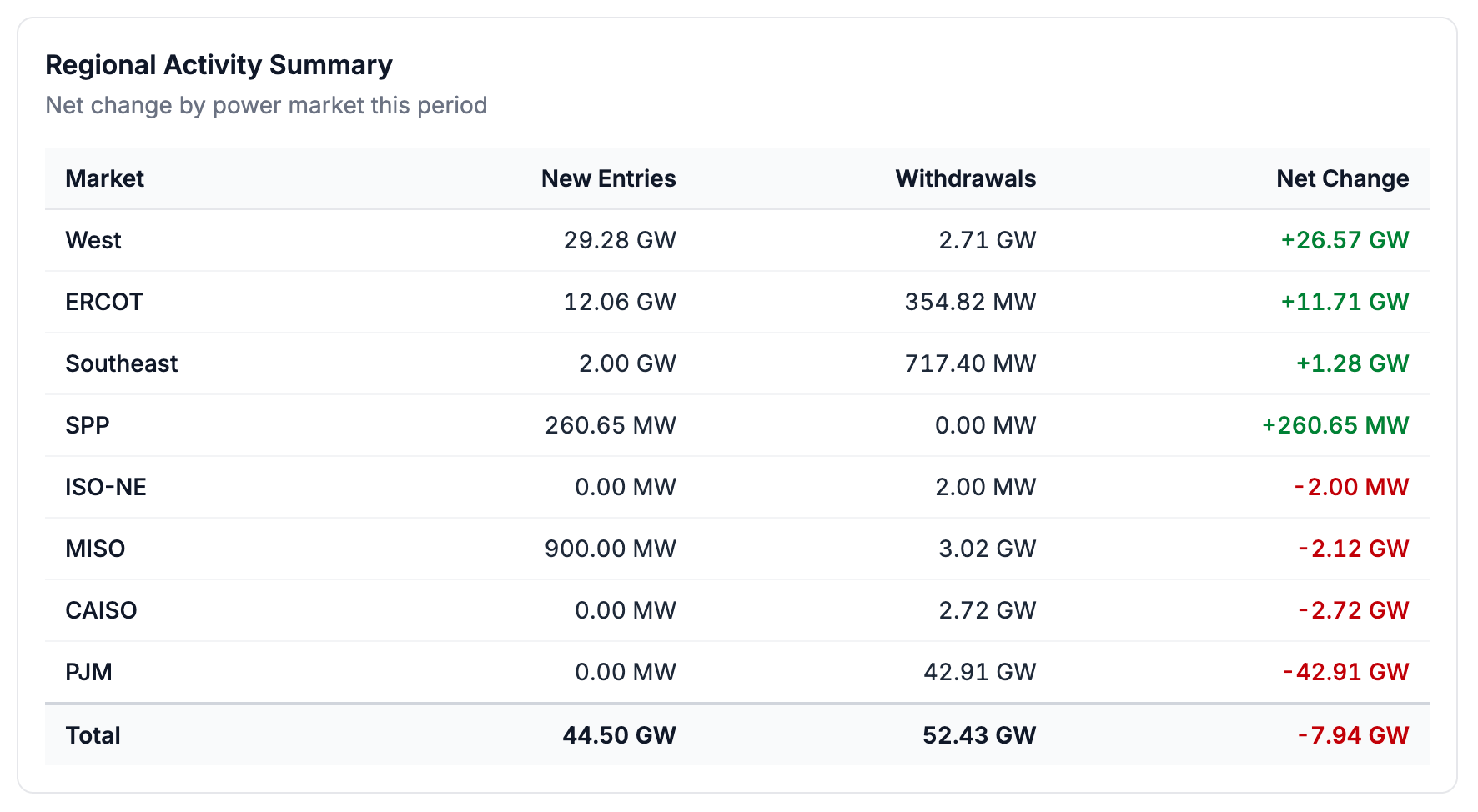

Withdrawals: 53.4 GW (384 projects)

Roughly 80% of all withdrawn capacity in this period is from PJM clearing out legacy, serial queue requests. Setting those aside, other withdrawals this period total 9.5 GW, and are concentrated in MISO and CAISO.

PJM: 42.9 GW (354 projects)

MISO: 3.0 GW (4 projects)

CAISO: 2.7 GW (10 projects)

Arizona Public Service: 2.0 GW (1 project)

Less than 1 GW of withdrawals in both ERCOT and the Southeast (Southern Company)

Additions: 44.5 GW (97 projects)

Arizona Public Service: 28.2 GW (58 projects)

ERCOT: 12.1 GW (26 projects)

Southeast: 2.0 GW (3 projects), all Duke Energy (Carolinas and Progress).

Outside the APS block, gas led the new requests (8.8 GW, 12 projects), ahead of storage (4.7 GW), a shift from the composition of new additions last period (solar+storage led the way last period).

In the News

America’s largest wind farm is now spinning. Pattern Energy brought its 3.65 GW SunZia project in New Mexico online, making it the largest wind farm in the country. A single 3.65 GW resource reaching operation is one of the larger commercial-operation milestones we expect to track all year, and a sign that some long-stalled western megaprojects are finally reaching the grid.

Big tech keeps building around the grid. Google and Intersect Power are developing the Meitner Energy Center in Texas, pairing a data center with more than a gigawatt of co-located wind, solar, storage, and on-site gas. It is their first project since Alphabet’s $4.75 billion acquisition of Intersect, and the co-located supply is meant to serve the data center’s load while limiting new demand on the local grid.

PJM opens a fast lane for shovel-ready generation. FERC has approved PJM’s expedited interconnection track, which will fast-track up to 10 projects a year for resources of at least 250 MW that can reach operation within three years. The carve-out runs through the end of 2027 and targets PJM’s resource adequacy needs as data center demand outpaces supply, with the first projects possibly named in October.

SPP gives large loads a conditional on-ramp. FERC approved SPP’s Conditional High-impact Large Load Service, letting large new loads such as data centers connect on a non-firm, interruptible basis until they secure firm resources or the needed network upgrades are finished. SPP says the structure gives developers more certainty on timing and cost. Alongside PJM’s fast lane, it shows RTOs improvising ways to absorb large loads in the near-term.

A Texas test case is setting the rules for co-located data centers. Crusoe, an AI data center developer, and the Goodnight wind farm asked regulators back in October to approve a net-metering deal that puts the data center behind the wind farm’s existing grid connection. ERCOT found no reliability problems but recommended approval only with strict curtailment terms, including a 30-minute shutdown during grid emergencies. The developer is contesting, and as one of the first contested cases under Senate Bill 6’s co-location policy, whatever the commission adopts will establish the template in ERCOT moving forward. It remains in contested hearings as of mid-June, with no ruling yet.

Activity Map

PJM accounts for the bulk of this period’s withdrawals, but based on our review of the data, covered in more detail below, we believe this is largely PJM clearing out older, stranded serial requests rather than active queue projects truly withdrawing. Outside of PJM, Arizona Public Service is driving new requests, while ERCOT shows a mix of new entries, withdrawals, newly operational projects, and newly signed GIAs.

Queue Activity

The two main figures this period, 44.5 GW (97 projects) of new entries and 52.4 GW (384 projects) of withdrawals, are each the product of a single-entity data event rather than a shift in the market.

Of the 52.4 GW of withdrawals, about 42.9 GW across 354 projects is PJM. Looking at the data, our assessment is that these withdrawals are clerical rather than formal withdrawals during this period. These are requests from PJM’s final serial queue intake windows, filed between 2021 and 2023 and nearly all still at the first study phase. We read this batch of withdrawals as PJM formally closing out its legacy serial queue as it moves to the cluster process, not as active projects leaving. The one exception worth noting is the Pilesgrove Solar project in New Jersey (149 MW), which is the only project in the group that progressed beyond the feasibility study phase and actually withdrew after executing an interconnection agreement.

That also means the technology split of this period’s withdrawals is an artifact of the cleanup rather than a signal about any resource. For example, 9.5 GW of offshore wind that withdrew in PJM this period comes from six serial requests being removed from the queue. We will be monitoring and reporting on the data from PJM’s Cycle 1 of the reformed process and will also cross-check the set of withdrawn PJM projects from this period against the new data once it drops.

Non-PJM withdrawals total roughly 7 GW this period, and are concentrated in MISO and CAISO. MISO lost roughly 3 GW, led by NIPSCO’s 1.1 GW Malden gas plant and a 1.5 GW CLECO request that withdrew prior to initiating the study phase. CAISO’s 2.7 GW of withdrawals across ten projects are all from the same April 2021 cluster, and withdrew during the System Impact Study stage, likely after receiving their study results and being required to commit additional deposits. A 2.0 GW APS request also dropped, though it dates to 2017 and carries no withdrawal date, so we suspect this is also the product of the utility doing some queue housekeeping.

New entries this period are inflated by a single source. APS accounts for 28.2 GW of the 44.5 GW across 58 projects. These requests have been accepted into APS’s queue but sit in deficiency review, meaning the submissions still need corrections, so their resource types and study details are not yet published. We expect that information to fill-in over the coming weeks and will analyze the batch properly once it does. The conventional new-entry activity is in ERCOT, which added 12.1 GW across 26 projects, and the Southeast, where Duke Energy added 2 GW. Among the new requests with populated resource type data, gas led at roughly 8.8 GW, ahead of storage at 4.7 GW.

Queue Snapshot - Current State

The active queue stands at 1.79 TW across 8,330 projects. Part of the decrease this period is the PJM cleanup working its way out of the active totals, and not an indication of developers losing interest in the region.

The more durable story is in the mix. Firm and dispatchable resources continue to gain ground, though the queue is still overwhelmingly solar and battery by volume. One caveat on the “Other” category, which is up three-fold to about 75 GW. Much of that growth is simply unclassified new entries like the APS batch that have not yet been assigned a technology, so it overstates how much genuinely uncategorized capacity is entering the queues.

Notable Projects

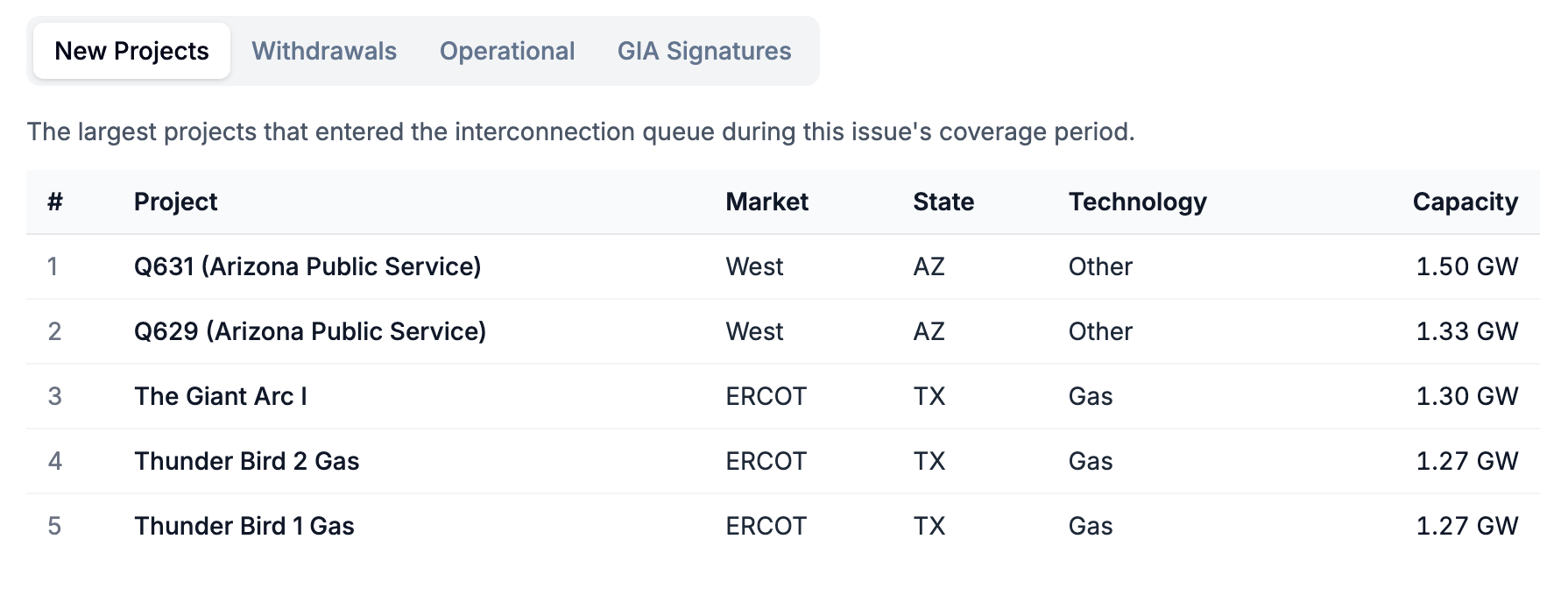

The largest projects this period are gas. There are gigawatt-scale gas plants entering the ERCOT queue, and the largest newly operational plant is gas as well. The largest withdrawals, as discussed above, are PJM cleaning up its queue rather than real cancellations.

At GridTracker, we are also tracking the data center buildout (existing data centers, permitting, and construction). Using this data, we find that the largest gas plants entering the queue are landing near existing or planned/proposed data center facilities. The Giant Arc I (1.3 GW) gas plant in Pecos County, TX is registered to an entity called Powering Knowledge, LLC (an opaque entity, but likely a shell company owned by a large energy or data center developer), and is located in the middle of a growing West Texas compute corridor. Within roughly 30 miles sit CoreWeave’s 250 MW site and Poolside AI’s 2 GW Project Horizon (currently under construction), with much larger proposed campuses from Microsoft (about 2.6 GW) and Pacifico Energy (the 7.65 GW GW Ranch) nearby. The same pattern appears to the north, where the two >1 GW Thunder Bird gas units in Jack County sit on the western edge of the Dallas-Fort Worth data center build-out. Though we cannot see the offtakers behind any of these projects, it looks like the firm capacity entering ERCOT’s queue is clustering near data center facilities.

At GridTracker, we are also tracking the data center buildout (existing data centers, permitting, and construction). Using this data, we find that the largest gas plants entering the queue are landing near existing or planned/proposed data center facilities.

The Giant Arc I (1.3 GW) gas plant in Pecos County, TX is registered to an entity called Powering Knowledge, LLC (an opaque entity, but likely a shell company owned by a large energy or data center developer), and is located in the middle of a growing West Texas compute corridor. Within roughly 30 miles sit CoreWeave's 250 MW site and Poolside AI's 2 GW Project Horizon (currently under construction), with much larger proposed campuses from Microsoft (about 2.6 GW) and Pacifico Energy (the 7.65 GW GW Ranch) nearby. The same pattern appears to the north, where the two >1 GW Thunder Bird gas units in Jack County sit on the western edge of the Dallas-Fort Worth data center build-out. Though we cannot see the offtakers behind any of these projects, it looks like the firm capacity entering ERCOT’s queue is clustering near data center facilities.

GridTracker users get access to:

Project-level insights (see the project-level changes that occur in real-time)

Exportable datasets (export the full list of newly operational, withdrawn, GIA-signed, and added projects)

Interactive graphs and visualizations

Custom dashboards with real-time alerts and data export

… and much more!

| A guest post by

|

| A guest post by

|